从零开始实现弹性网络回归

先决条件:

- 线性回归

- 梯度下降

- 套索和岭回归

介绍:

Elastic-Net 回归是线性回归的修改,它共享相同的预测假设函数。线性回归的成本函数由J表示。

Here, m is the total number of training examples in the dataset.

h(x(i)) represents the hypothetical function for prediction.

y(i) represents the value of target variable for ith training example.

线性回归存在过拟合问题,无法处理共线数据。当数据集中有许多特征,甚至其中一些与预测模型无关时。这使得模型更加复杂,对测试集的预测过于不准确(或过度拟合)。这种具有高方差的模型不能对新数据进行泛化。因此,为了处理这些问题,我们同时包含 L-2 和 L-1 范数正则化,以同时获得 Ridge 和 Lasso 的好处。结果模型比 Lasso 具有更好的预测能力。它执行特征选择,也使假设更简单。 Elastic-Net 回归的修正成本函数如下所示:

![\frac{1}{m}\left[\sum_{l=1}^{m}\left(y^{(i)}-h\left(x^{(i)}\right)\right)^{2}+\lambda_{1} \sum_{j=1}^{n} w_{j}+\lambda_{2} \sum_{j=1}^{n} w_{j}^{2}\right]](https://mangodoc.oss-cn-beijing.aliyuncs.com/geek8geeks/Implementation_of_Elastic_Net_Regression_From_Scratch_1.png "由 QuickLaTeX.com 渲染")

Here, w(j) represents the weight for jth feature.

n is the number of features in the dataset.

lambda1 is the regularization strength for L-1 norm.

lambda2 is the regularization strength for L-2 norm.数学直觉:

在其成本函数的梯度下降优化过程中,添加 L-2 惩罚项导致模型的权重降低到接近于零。由于权重的惩罚,假设变得更简单、更通用,并且不太容易过度拟合。添加了接近零或零的 L1 惩罚权重。那些缩小到零的权重消除了假设函数中存在的特征。因此,不相关的特征不参与预测模型。权重的这种惩罚使假设更具预测性,从而促进了稀疏性(具有少量参数的模型)。

调整 lambda1 和 lamda2 值的不同情况。

- 如果 lambda1 和 lambda2 设置为 0,则 Elastic-Net 回归等于线性回归。

- 如果 lambda1 设置为 0,则 Elastic-Net 回归等于岭回归。

- 如果 lambda2 设置为 0,则 Elastic-Net 回归等于 Lasso 回归。

- 如果将 lambda1 和 lambda2 设置为无穷大,则所有权重都缩小为零

因此,我们应该将 lambda1 和 lambda2 设置在 0 和无穷大之间。

执行:

此实现中使用的数据集可以从链接下载。

它有 2 列——“ YearsExperience ”和“ Salary ”,用于一家公司的 30 名员工。因此,在此,我们将训练一个 Elastic-Net Regression 模型来学习每个员工的工作年限与他们各自的薪水之间的相关性。一旦模型训练好,我们就可以根据员工多年的经验来预测他的薪水。

代码:

# Importing libraries

import numpy as np

import pandas as pd

from sklearn.model_selection import train_test_split

import matplotlib.pyplot as plt

# Elastic Net Regression

class ElasticRegression() :

def __init__( self, learning_rate, iterations, l1_penality, l2_penality ) :

self.learning_rate = learning_rate

self.iterations = iterations

self.l1_penality = l1_penality

self.l2_penality = l2_penality

# Function for model training

def fit( self, X, Y ) :

# no_of_training_examples, no_of_features

self.m, self.n = X.shape

# weight initialization

self.W = np.zeros( self.n )

self.b = 0

self.X = X

self.Y = Y

# gradient descent learning

for i in range( self.iterations ) :

self.update_weights()

return self

# Helper function to update weights in gradient descent

def update_weights( self ) :

Y_pred = self.predict( self.X )

# calculate gradients

dW = np.zeros( self.n )

for j in range( self.n ) :

if self.W[j] > 0 :

dW[j] = ( - ( 2 * ( self.X[:,j] ).dot( self.Y - Y_pred ) ) +

self.l1_penality + 2 * self.l2_penality * self.W[j] ) / self.m

else :

dW[j] = ( - ( 2 * ( self.X[:,j] ).dot( self.Y - Y_pred ) )

- self.l1_penality + 2 * self.l2_penality * self.W[j] ) / self.m

db = - 2 * np.sum( self.Y - Y_pred ) / self.m

# update weights

self.W = self.W - self.learning_rate * dW

self.b = self.b - self.learning_rate * db

return self

# Hypothetical function h( x )

def predict( self, X ) :

return X.dot( self.W ) + self.b

# Driver Code

def main() :

# Importing dataset

df = pd.read_csv( "salary_data.csv" )

X = df.iloc[:,:-1].values

Y = df.iloc[:,1].values

# Splitting dataset into train and test set

X_train, X_test, Y_train, Y_test = train_test_split( X, Y,

test_size = 1/3, random_state = 0 )

# Model training

model = ElasticRegression( iterations = 1000,

learning_rate = 0.01, l1_penality = 500, l2_penality = 1 )

model.fit( X_train, Y_train )

# Prediction on test set

Y_pred = model.predict( X_test )

print( "Predicted values ", np.round( Y_pred[:3], 2 ) )

print( "Real values ", Y_test[:3] )

print( "Trained W ", round( model.W[0], 2 ) )

print( "Trained b ", round( model.b, 2 ) )

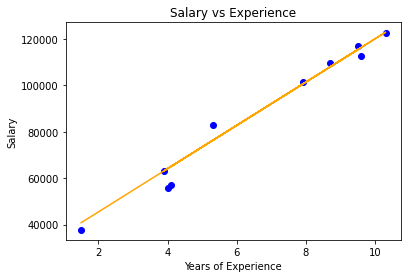

# Visualization on test set

plt.scatter( X_test, Y_test, color = 'blue' )

plt.plot( X_test, Y_pred, color = 'orange' )

plt.title( 'Salary vs Experience' )

plt.xlabel( 'Years of Experience' )

plt.ylabel( 'Salary' )

plt.show()

if __name__ == "__main__" :

main()

输出:

Predicted values [ 40837.61 122887.43 65079.6 ]

Real values [ 37731 122391 57081]

Trained W 9323.84

Trained b 26851.84

弹性网络模型可视化

注意: Elastic-Net 回归自动执行模型选择的某些部分并导致降维,这使其成为计算高效的模型。