R 编程中的正则化

正则化是一种回归技术,可将系数估计缩小或正则化或约束到 0(或零)。在这种技术中,为了降低给定模型的自由度,对模型的各种参数添加了惩罚。正则化的概念大致可以分为:

- 岭回归

- 套索回归

- 弹性网络回归

R中的实现

在 R 语言中,要执行正则化,我们需要在开始处理它们之前安装一些包。所需的软件包是

- 用于岭回归和套索回归的glmnet包

- 用于数据清理的dplyr包

- psych包,用于执行或计算矩阵的跟踪函数

- 插入符号包

要安装这些包,我们必须使用 R 控制台中的install.packages() 。成功安装包后,我们使用library()命令将这些包包含在我们的 R 脚本中。为了实现正则化回归技术,我们需要遵循三种正则化技术中的任何一种。

岭回归

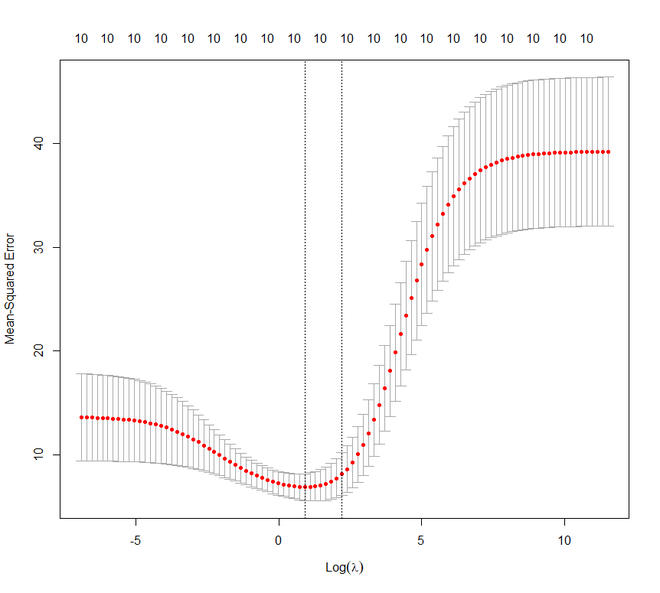

岭回归是线性回归的修改版本,也称为L2 正则化。与线性回归不同,损失函数被修改以最小化模型的复杂性,这是通过添加一些惩罚参数来完成的,该惩罚参数相当于系数值或大小的平方。基本上,要在 R 中实现岭回归,我们将使用“ glmnet ”包。 cv.glmnet()函数将用于确定岭回归。

例子:

在这个例子中,我们将在mtcars数据集上实现岭回归技术,以获得更好的说明。我们的任务是根据汽车的其他特性预测每加仑行驶里程。我们将使用set.seed()函数来设置种子以实现可重复性。我们将通过三种方式设置 lambda 的值:

- 通过执行 10 折交叉验证

- 基于得到的信息

- 基于这两个标准的最佳 lambda

R

# Regularization

# Ridge Regression in R

# Load libraries, get data & set

# seed for reproducibility

set.seed(123)

library(glmnet)

library(dplyr)

library(psych)

data("mtcars")

# Center y, X will be standardized

# in the modelling function

y <- mtcars %>% select(mpg) %>%

scale(center = TRUE, scale = FALSE) %>%

as.matrix()

X <- mtcars %>% select(-mpg) %>% as.matrix()

# Perform 10-fold cross-validation to select lambda

lambdas_to_try <- 10^seq(-3, 5, length.out = 100)

# Setting alpha = 0 implements ridge regression

ridge_cv <- cv.glmnet(X, y, alpha = 0,

lambda = lambdas_to_try,

standardize = TRUE, nfolds = 10)

# Plot cross-validation results

plot(ridge_cv)

# Best cross-validated lambda

lambda_cv <- ridge_cv$lambda.min

# Fit final model, get its sum of squared

# residuals and multiple R-squared

model_cv <- glmnet(X, y, alpha = 0, lambda = lambda_cv,

standardize = TRUE)

y_hat_cv <- predict(model_cv, X)

ssr_cv <- t(y - y_hat_cv) %*% (y - y_hat_cv)

rsq_ridge_cv <- cor(y, y_hat_cv)^2

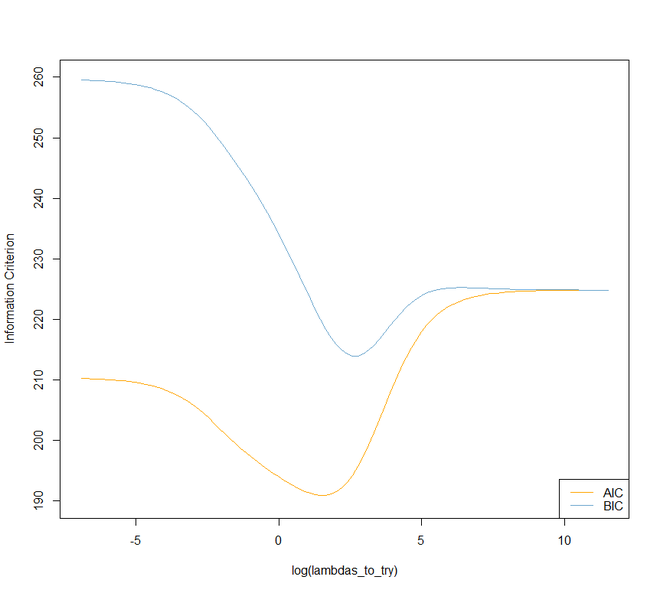

# selecting lambda based on the information

X_scaled <- scale(X)

aic <- c()

bic <- c()

for (lambda in seq(lambdas_to_try))

{

# Run model

model <- glmnet(X, y, alpha = 0,

lambda = lambdas_to_try[lambda],

standardize = TRUE)

# Extract coefficients and residuals (remove first

# row for the intercept)

betas <- as.vector((as.matrix(coef(model))[-1, ]))

resid <- y - (X_scaled %*% betas)

# Compute hat-matrix and degrees of freedom

ld <- lambdas_to_try[lambda] * diag(ncol(X_scaled))

H <- X_scaled %*% solve(t(X_scaled) %*% X_scaled + ld)

%*% t(X_scaled)

df <- tr(H)

# Compute information criteria

aic[lambda] <- nrow(X_scaled) * log(t(resid) %*% resid)

+ 2 * df

bic[lambda] <- nrow(X_scaled) * log(t(resid) %*% resid)

+ 2 * df * log(nrow(X_scaled))

}

# Plot information criteria against tried values of lambdas

plot(log(lambdas_to_try), aic, col = "orange", type = "l",

ylim = c(190, 260), ylab = "Information Criterion")

lines(log(lambdas_to_try), bic, col = "skyblue3")

legend("bottomright", lwd = 1, col = c("orange", "skyblue3"),

legend = c("AIC", "BIC"))

# Optimal lambdas according to both criteria

lambda_aic <- lambdas_to_try[which.min(aic)]

lambda_bic <- lambdas_to_try[which.min(bic)]

# Fit final models, get their sum of

# squared residuals and multiple R-squared

model_aic <- glmnet(X, y, alpha = 0, lambda = lambda_aic,

standardize = TRUE)

y_hat_aic <- predict(model_aic, X)

ssr_aic <- t(y - y_hat_aic) %*% (y - y_hat_aic)

rsq_ridge_aic <- cor(y, y_hat_aic)^2

model_bic <- glmnet(X, y, alpha = 0, lambda = lambda_bic,

standardize = TRUE)

y_hat_bic <- predict(model_bic, X)

ssr_bic <- t(y - y_hat_bic) %*% (y - y_hat_bic)

rsq_ridge_bic <- cor(y, y_hat_bic)^2

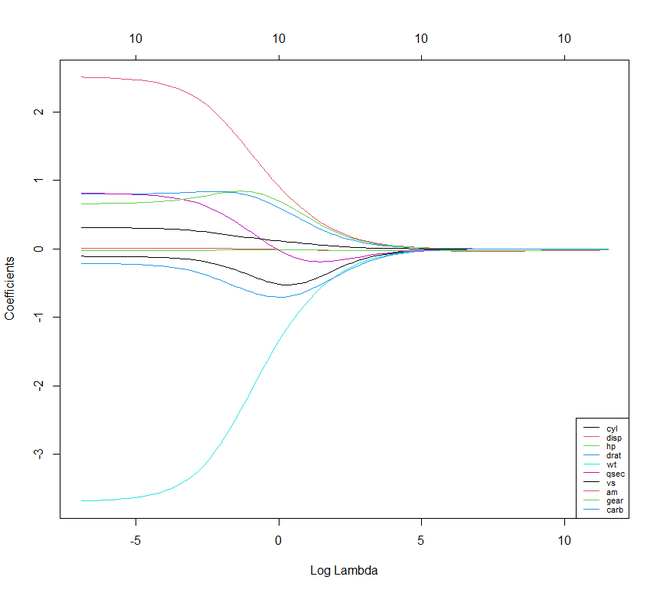

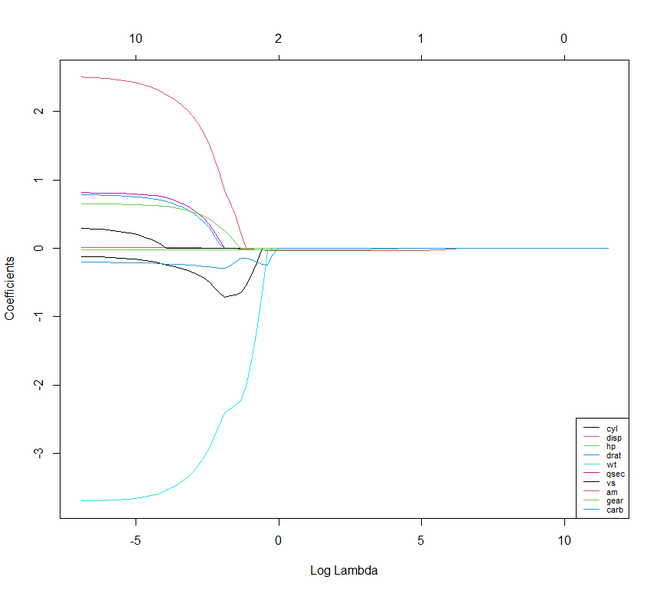

# The higher the lambda, the more the

# coefficients are shrinked towards zero.

res <- glmnet(X, y, alpha = 0, lambda = lambdas_to_try,

standardize = FALSE)

plot(res, xvar = "lambda")

legend("bottomright", lwd = 1, col = 1:6,

legend = colnames(X), cex = .7)R

# Regularization

# Lasso Regression

# Load libraries, get data & set

# seed for reproducibility

set.seed(123)

library(glmnet)

library(dplyr)

library(psych)

data("mtcars")

# Center y, X will be standardized in the modelling function

y <- mtcars %>% select(mpg) %>% scale(center = TRUE,

scale = FALSE) %>%

as.matrix()

X <- mtcars %>% select(-mpg) %>% as.matrix()

# Perform 10-fold cross-validation to select lambda

lambdas_to_try <- 10^seq(-3, 5, length.out = 100)

# Setting alpha = 1 implements lasso regression

lasso_cv <- cv.glmnet(X, y, alpha = 1,

lambda = lambdas_to_try,

standardize = TRUE, nfolds = 10)

# Plot cross-validation results

plot(lasso_cv)

# Best cross-validated lambda

lambda_cv <- lasso_cv$lambda.min

# Fit final model, get its sum of squared

# residuals and multiple R-squared

model_cv <- glmnet(X, y, alpha = 1, lambda = lambda_cv,

standardize = TRUE)

y_hat_cv <- predict(model_cv, X)

ssr_cv <- t(y - y_hat_cv) %*% (y - y_hat_cv)

rsq_lasso_cv <- cor(y, y_hat_cv)^2

# The higher the lambda, the more the

# coefficients are shrinked towards zero.

res <- glmnet(X, y, alpha = 1, lambda = lambdas_to_try,

standardize = FALSE)

plot(res, xvar = "lambda")

legend("bottomright", lwd = 1, col = 1:6,

legend = colnames(X), cex = .7)R

# Regularization

# Elastic Net Regression

library(caret)

# Set training control

train_control <- trainControl(method = "repeatedcv",

number = 5,

repeats = 5,

search = "random",

verboseIter = TRUE)

# Train the model

elastic_net_model <- train(mpg ~ .,

data = cbind(y, X),

method = "glmnet",

preProcess = c("center", "scale"),

tuneLength = 25,

trControl = train_control)

# Check multiple R-squared

y_hat_enet <- predict(elastic_net_model, X)

rsq_enet <- cor(y, y_hat_enet)^2

print(y_hat_enet)

print(rsq_enet)输出:

套索回归

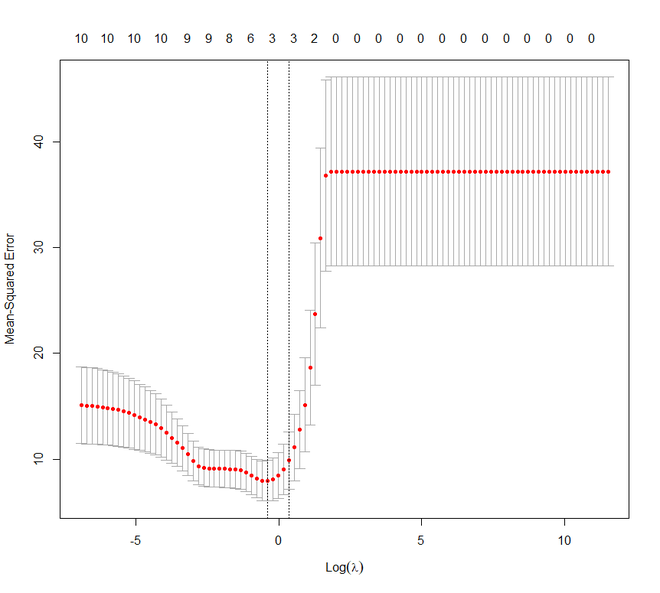

前进到Lasso 回归。它也被称为L1 回归、选择算子和最小绝对收缩。它也是线性回归的修改版本,其中再次修改了损失函数以最小化模型的复杂性。这是通过限制模型系数的绝对值的总和来完成的。在 R 中,我们可以使用与岭回归相同的“ glmnet ”包来实现套索回归。

例子:

在此示例中,我们再次使用mtcars数据集。在这里,我们还将像前面的示例一样设置 lambda 值。

R

# Regularization

# Lasso Regression

# Load libraries, get data & set

# seed for reproducibility

set.seed(123)

library(glmnet)

library(dplyr)

library(psych)

data("mtcars")

# Center y, X will be standardized in the modelling function

y <- mtcars %>% select(mpg) %>% scale(center = TRUE,

scale = FALSE) %>%

as.matrix()

X <- mtcars %>% select(-mpg) %>% as.matrix()

# Perform 10-fold cross-validation to select lambda

lambdas_to_try <- 10^seq(-3, 5, length.out = 100)

# Setting alpha = 1 implements lasso regression

lasso_cv <- cv.glmnet(X, y, alpha = 1,

lambda = lambdas_to_try,

standardize = TRUE, nfolds = 10)

# Plot cross-validation results

plot(lasso_cv)

# Best cross-validated lambda

lambda_cv <- lasso_cv$lambda.min

# Fit final model, get its sum of squared

# residuals and multiple R-squared

model_cv <- glmnet(X, y, alpha = 1, lambda = lambda_cv,

standardize = TRUE)

y_hat_cv <- predict(model_cv, X)

ssr_cv <- t(y - y_hat_cv) %*% (y - y_hat_cv)

rsq_lasso_cv <- cor(y, y_hat_cv)^2

# The higher the lambda, the more the

# coefficients are shrinked towards zero.

res <- glmnet(X, y, alpha = 1, lambda = lambdas_to_try,

standardize = FALSE)

plot(res, xvar = "lambda")

legend("bottomright", lwd = 1, col = 1:6,

legend = colnames(X), cex = .7)

输出:

如果我们比较 Lasso 和 Ridge 回归技术,我们会注意到这两种技术或多或少是相同的。但是它们之间几乎没有什么不同的特征。

- 与 Ridge 不同,Lasso 可以将其某些参数设置为零。

- 在岭中,相关的预测变量的系数是相似的。而在套索中,只有一个预测系数较大,其余的趋于零。

- 如果存在许多具有相同值的巨大或大参数,则 Ridge 效果很好。如果仅存在少量确定或重要的参数并且其余参数趋于零,则套索可以很好地工作。

弹性网络回归

我们现在将继续讨论弹性网络回归。弹性网络回归可以说是套索和岭回归的凸组合。我们甚至可以在这里使用glmnet包。但是现在我们将看到如何使用包插入符号来实现弹性网络回归。

例子:

R

# Regularization

# Elastic Net Regression

library(caret)

# Set training control

train_control <- trainControl(method = "repeatedcv",

number = 5,

repeats = 5,

search = "random",

verboseIter = TRUE)

# Train the model

elastic_net_model <- train(mpg ~ .,

data = cbind(y, X),

method = "glmnet",

preProcess = c("center", "scale"),

tuneLength = 25,

trControl = train_control)

# Check multiple R-squared

y_hat_enet <- predict(elastic_net_model, X)

rsq_enet <- cor(y, y_hat_enet)^2

print(y_hat_enet)

print(rsq_enet)

输出:

> print(y_hat_enet)

Mazda RX4 Mazda RX4 Wag Datsun 710 Hornet 4 Drive Hornet Sportabout Valiant

2.13185747 1.76214273 6.07598463 0.50410531 -3.15668592 0.08734383

Duster 360 Merc 240D Merc 230 Merc 280 Merc 280C Merc 450SE

-5.23690809 2.82725225 2.85570982 -0.19421572 -0.16329225 -4.37306992

Merc 450SL Merc 450SLC Cadillac Fleetwood Lincoln Continental Chrysler Imperial Fiat 128

-3.83132657 -3.88886320 -8.00151118 -8.29125966 -8.08243188 6.98344302

Honda Civic Toyota Corolla Toyota Corona Dodge Challenger AMC Javelin Camaro Z28

8.30013895 7.74742320 3.93737683 -3.13404917 -2.56900144 -5.17326892

Pontiac Firebird Fiat X1-9 Porsche 914-2 Lotus Europa Ford Pantera L Ferrari Dino

-4.02993835 7.36692700 5.87750517 6.69642869 -2.02711333 0.06597788

Maserati Bora Volvo 142E

-5.90030273 4.83362156

> print(rsq_enet)

[,1]

mpg 0.8485501